Dear IReeN Members

We trust you are all keeping well.

As you are aware, the Coronavirus Job Retention Scheme (CJRS) closed at the end of September and as lockdown eases across the UK and employees are gradually returning to their offices.

In today’s newsletter, we wanted to highlight a few snippets of important news but there are further details and regular news items on our website www.ireen.net

Virtual National meeting 20th January 2022

The committee was planning to host another virtual meeting for members during 2021. However, our colleagues at HMRC have suggested that there will be more news to share in January, so we progressing a virtual meeting for members on 20th January 2022.

To book your place:

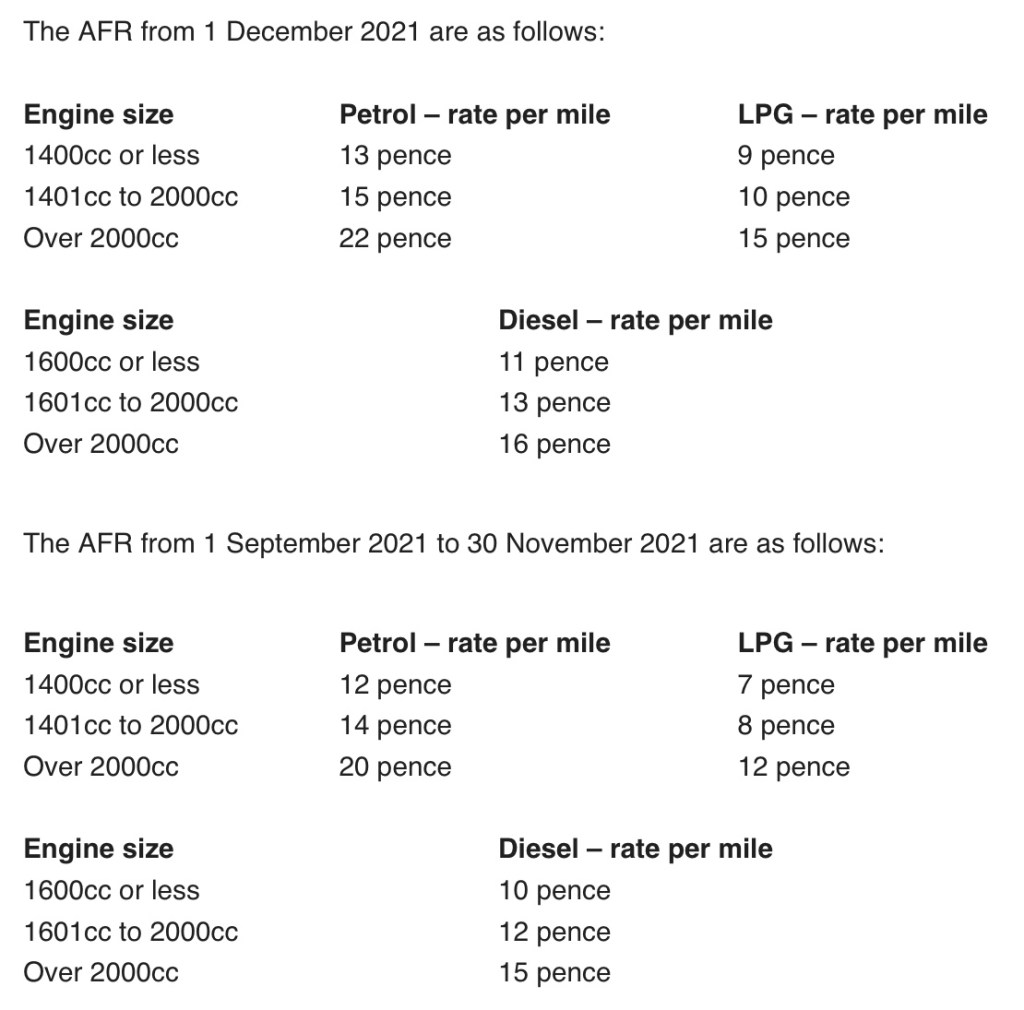

Advisory Fuel Rates from 1st December 2021

HMRC review and publish the Advisory Fuel Rates (AFR) for company cars on a quarterly basis in March, June, September, and December each year.

The Advisory Fuel Rates from 1 September 2021, were published at the end of August and the new rates for December were published on 24th November 2021. Both sets of rates are set out below.

Employers can use the previously published rates for up to one month after the rates change if they wish.

The mileage rates for fully electric cars continue to be 4p per mile. Hybrid cars use either the diesel or petrol rates as appropriate.

The AFR is used for company cars where:

- The employer is reimbursing the employee for business travel

- The employee is repaying the cost of private travel in a company car

No fuel benefit charge will arise, providing all private travel mileage is correctly recorded. The correct rate (or higher) must be used to calculate how much an employee must repay their employer for fuel used for private travel.

SSP Rebate Scheme Closed

The Coronavirus Job Retention Scheme has now closed and the deadline for making adjustments (28 October 2021 has now passed).

Although the Statutory Sick Pay (SSP) Rebate Scheme closed on 30 September 2021. Employers have until 31 December 2021 to submit any final claims for SSP rebates.

The SSP Rebate Scheme only applied to small and medium-sized employers, defined as those with less than 250 employees. They can reclaim up to two weeks SSP per employee where the sickness absence was due to Covid-19 or self-isolation. It does not apply to individuals going into quarantine following a trip abroad unless they satisfy other qualifying conditions such as an isolation note from NHS 111.

To qualify for the SSP rebate, the absence must last for four or more consecutive calendar days and the absence was up to 30 September 2021.

Where the sickness absence (up to 30 September 2021) was Covid-19 related, the waiting days for SSP purposes are suspended and therefore SSP can be paid from the first qualifying day.

If an employer is reclaiming SSP, he is obliged to keep SSP records for 3 years plus the current tax year.

Compulsory Covid-19 Vaccinations for Care Workers

A controversial new law came into force on 11 November 2021 which will require care workers to be fully vaccinated against Covid-19.

The new regulations impose the requirement for compulsory vaccination of care workers in accordance with the Public Health (Control of Disease) Act 1094 under section 45C. Although it is claimed that this is in contravention of section 45E which excludes medical treatment such as vaccinations.

Many care workers have raised their concerns. A formal judicial review proceeding is expected shortly, which will challenge the Care Home Regulations.

Relaxation of Right to Work Checks Extended

The government recently announced that they will be extending the temporary adjusted checks regarding the right to work checks (which were due to end on 31 August 2021) until 5 April 2022. The temporary adjustments of video interviews with prospective employees and the acceptance of scanned documents prove the right to work in the UK.

From 1 September 2021 employers were initially going to be required to return to face-to-face interviews and only accept original documents. But the Home Office decided to extend the temporary arrangement until the end of the current tax year to provide employers with additional support.

This is a further change to the new guidance which was originally published on 18 June 2021 and the employer checklist published at the beginning of July 2021.

The Home Office will publish further guidance in advance of the 5th April 2022 deadline.

Employers are advised to use the Home Office Employer Checking Service if a prospective or existing employee cannot provide any of the accepted documents that are listed in the guidance.

Veteran NIC Holiday – further details

HMRC Software Developers Team (SDT) has now published further guidance to software developers regarding the employer’s NIC Holiday for Veterans.

The NIC Holiday for Veterans will provide a zero rate of secondary Class 1 National Insurance contributions on the earnings of qualifying veterans of the armed forces for 12 consecutive months. The 12 consecutive months begins from the first day of civilian employment after leaving the regular armed forces, between 6 April 2021 until March 2022.

Employers can claim the relief for 12 months and is a set period. The set period is unaffected if the employment ceases for any reason.

However, if a subsequent employer, employs the veteran within the qualifying period they will be eligible to claim the relief for the remainder of the set period as applicable. But to determine when the first day of civilian employment began, the subsequent employer must establish when the first day of civilian employment with the previous employer occurred.

Employers who want to claim the veteran’s NIC relief will have to pay secondary NI contributions in the normal way for 2021/22 and then reclaim the veteran’s NIC relief the following tax year i.e. 2022/23.

Who Qualifies?

Eligible veterans are defined as those who have served at least one day in the regular armed forces, and this includes those who have only completed one day of basic training. It doesn’t matter when the veteran left the armed forces providing this is their first civilian employment (or subsequent employment which falls in the qualifying set period).

The Calculations

The Veterans’ NIC Holiday will be applied at a zero rate, on earnings above the Secondary Threshold up to the new Veterans Upper Secondary Threshold (VUST). Where the veteran’s earnings exceed the VUST, Secondary contributions will be due on the excess above the VUST. Primary national insurance contributions are unaffected.

New Category Letter

There will be a new veteran’s NI category letter “V” which will mirror the existing NI category letter A.

However, rare cases may arise where the veteran would normally be on another NI category letter: B, T, C, W, J and Q but there is no veteran’s equivalent letter. For these rare occurrences, employers are advised to apply the existing standard category for the duration of the tax year and to contact HMRC at tax year-end for advice. HMRC will be able to guide the employer through the manual process for making the adjustment outside of their payroll software solution.

For further details see our article on to www.ireen.net

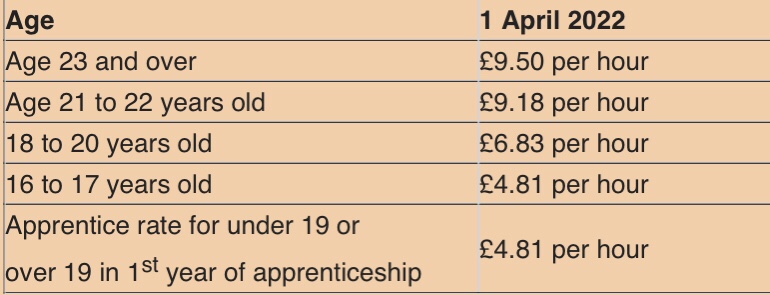

NMW Rates Confirmed for April 2022

The new NLW and NMW rates for 2022 for those aged under 23 have now been confirmed and the new rates are as follows and increase from 1 April 2022:

Voluntary Living Wage increases

The Living Wage Foundation confirmed on 15 November 2021 that the Living Wage rates would increase from 15 November 2021.

The new rates are:

- £9.90 per hour for those aged 18 and above for outside London and

- £11.05 per hour for the London area.

Unlike the National Living Wage, the Living Wage is optional. It applies to the employers who have signed up for the Living Wage Foundation’s accredited scheme of nearly 9,000 employers.

Members of the accreditation scheme normally have up to six months to implement the increase to the hourly rates.

New Health & Social Care Levy

As a result of the Government’s recent announcement regarding the introduction of a 1.25% increase to national insurance contributions (Primary and Secondary) for 2022/23 to provide for social care, HMRC has now published further details of the proposal in their policy paper.

NI increase is a temporary measure

The increase in NI is a temporary measure and will apply for 2022/23 only and will affect Class 1, Class 1A and Class 1B plus Class 4 for the self-employed.

The levy will be paid by the employed and self-employed where their earnings fall above the Primary Threshold (Class 1) and the Lower Profits Limit (Class 4). For example, an employee earning a salary of £24,100 p.a. will pay an additional £180. Whereas an individual earning on a salary of £67,100 per annum will pay an additional £715.

How it will work

The temporary increase of 1.25% will apply to Class 1, Class 1A, Class 1B and Class 4 national insurance contributions for 2022/23 tax year and will apply to all parts of the UK.

With effect from 6th April 2023 the national insurance rates will revert to 2021/22 level and the increase of 1.25 percent will be replaced with a 1.25 percent Health and Social Care Levy.

Although individuals over state pension age that are still working will not be affected by the 1.25% increase to national insurance contributions, they will be liable for the Health and Social Care Levy from 6th April 2023.

For details of HMRC’s policy paper Budget and 2022/23

Many of the new rates and thresholds for 2022/23 were confirmed on Budget day and they are set out below. However, the Scottish and Welsh tax rates have not yet been confirmed.

2022-23

Personal Allowance: £12,570

PAYE Thresholds: Weekly: £242; Monthly: £1,048

Standard / Emergency tax code: 1257L

Tax Code uplifts:

L: N/A due to no change in the Personal Allowance

M: N/A due to no change in the Personal Allowance

N: N/A due to no change in the Personal Allowance

Income Tax Rates – England & Northern Ireland (rUK)

Income Tax Rates – Scotland

Income Tax Rates – Wales

Awaiting confirmation from the Welsh Assembly.

Class 1 NICs rates and thresholds 2022/23:

The new Health and Social Care Levy of 1.25% will be applied to Class 1, Class 1A and Class 1B rates for 2022/23 only.

The rates and thresholds for 2022/23 for Class 1 NI are attached.

Class 1A NICs rate: 15.05%

Class 1B NICs rate: 15.05%

Student Loan & Postgraduate Loan Thresholds and deduction rates:

Student Loan Plan 1 £20,195 @ 9%

Student Loan Plan 2 TBA

Student Loan Plan 4 £25,375 @ 9% (Scottish Student Loan)

Postgraduate Loan TBA

Employment Allowance:

Continues to be up to £4,000

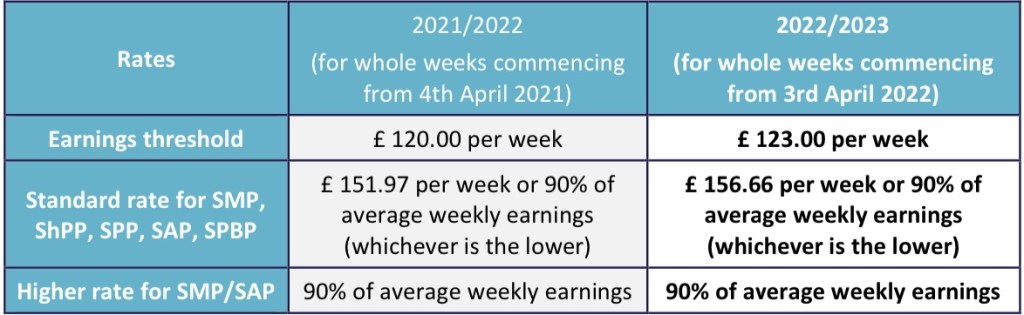

Statutory Payments rates:

Statutory Maternity, Paternity, Adoption, Shared Parental and Parental Bereavement Pay

Use the maternity, adoption and paternity calculator for employers to calculate your employee’s:

- Statutory Maternity Pay (SMP)

- paternity or adoption pay

- qualifying week

- average weekly earnings

- leave period

These rates apply from 3 April 2022.

Statutory Sick Pay (SSP)

The same weekly SSP rate applies to all employees. However, the amount you must actually pay an employee for each day they’re off work due to illness (the daily rate) depends on the number of ‘qualifying days’ they work each week.

Use the SSP calculator to work out your employee’s sick pay, or use these rates.

These rates apply from 6 April 2022.

Apprenticeship Levy:

£15,000 offset allowance

Rate 0.5%